The people in the Middle East are no strangers to boycotting products and services that come in direct conflict with their values. During the boycott campaigns, consumers tend to fight producers and service providers that directly or indirectly show solidarity to causes that contradict theirs by consuming localized alternatives. Muslim communities for example, have boycotted Danish FMCG products in 2005 and 2006 because of the publication of an insulting cartoon of the prophet Muhammed (Peace be upon him). A similar campaign because of similar actions taken by French media in 2008 which led to the boycott of French products in the Middle East including Kuwait. The boycotts have resulted in significant financial impact on Danish and French companies during the two events. According to a press release by Arla Foods (Danish-Swedish Dairy Company), the company sustained a 60 million USD loss in 2006 as a result of the boycott of their products in the Muslim majority countries, especially in the Middle East.

The war erupted on the 7th of October which was followed by one week of market and consumer shock that companies and brands did not take sides. Taking sides started being reported in the news and social media one week after the incident where the Israel franchisors and international brands showed solidarity and support to the Israel Defense Forces (IDF) by offering meals, drinks, products, and/or financial support. Such reported news ignited massive consumer protests worldwide and mainly in the Middle East. Those brands that are present in this region were heavily criticized and called out. The consumer boycott movement by users of social media platforms started picking up in the third week of October and then was adopted by regular consumers. Brands started witnessing a slowdown in footfall in the third week of October and it became clear that the general public has taken a strong stance against the brands in question.

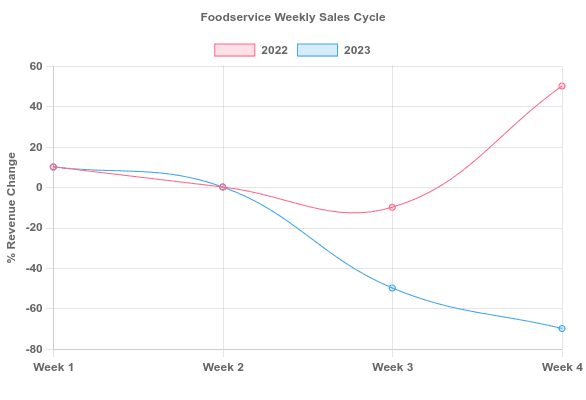

From the third week of October, the affected brands are the major leading brands in terms of market share and market penetration. These brands have been operating in the local markets since the 1990s and have grown their market share to dominate the other players for decades now. The consumer foodservice culture and habits is actually shaped by these brands. The current seismic market impact of this conflict is more severe in consequence than the COVID impact. Consumer loyalty and brand trust was not in question during the COVID lockdowns but rather forced market slowdown due to unprecedented health panic. The semi-independent social initiatives undertaken by the franchisors in the region were seen as a brand initiative to support one side over the other. For example, brands offered free meals to the IDF while the same brands in Middle Eastern and Muslim majority countries donated money to support the humanitarian efforts in Gaza. Additionally, the Middle Eastern social media movements have been active in shedding light on the historic political siding of these brands and how they have been dealing with the Palestinian conflict for the past 70 years. Such exposure led to deeper community mistrust and therefore has affected their performances. Consumer spending in foodservice venues is trendy during any month towards spending more in the fourth and first week of the month as a result of salaries and paychecks being paid out during that period. October was no different except for the fact that sales have taken a turn in the third week and took a nose dive in the fourth week of the month. According to the primary research undertaken by Global Markets, the leading global foodservice brands that were outcasted have witnessed a drop in their sales in the fourth week of October 70% on average compared to October of 2022.

Many speculated that local brands have absorbed the lost market share of the leading international brands during October, the answer is yes and no. First, the leading international brands in question are leading the market by 2 to 4 time the performance for their direct competitors in the second and third market share position. Such market superiority is derived from their market penetration in outlet count and outlet positioning that is offering the right products and prices at their consumer’s finger tips either through their apps or through their drive-thru stores. Such convenience in price and proximity is not applicable to their competitors even those who follow in the second market share position. Local and international brands who come in the second and third share position have gained between 5% to 15% market share while the smaller players barely witnessed any growth.

Looking at the previous boycott movements, the boycott is expected to last 1 to 3 months longer than the war if not 6 months due to the severity and humanitarian impact of this conflict.

As a result of the boycott campaign on social media platforms, the affected brands reacted immediately by issuing statements and press releases to distance themselves from the brands’ actions that caused the controversy. However, those damage control statements didn’t help much and caused more backlash from social media users, to the point where the brands had to disable the comment section to their posts in this regard.

It is highly unlikely that the leading burger and coffee brands to shut down in any of the Middle Eastern and Muslim majority countries due to the market penetration factors highlighted above. Their market shares however are expected to shrink in the short term and it will be difficult to regain them from the direct competitors. The brands have to work very hard to rebuild their market image which therefore would regain their market share. It is clear that in the globalized economy and connected consumer world is important to draw a line between social, religious, and political stance with the product and service you sell. and A 30 year social and brand buildup efforts can be destroyed in one meal box donated to your political enemy.

;

; ;

;